Nicolas Frendo – CFO – 4 Minute Read

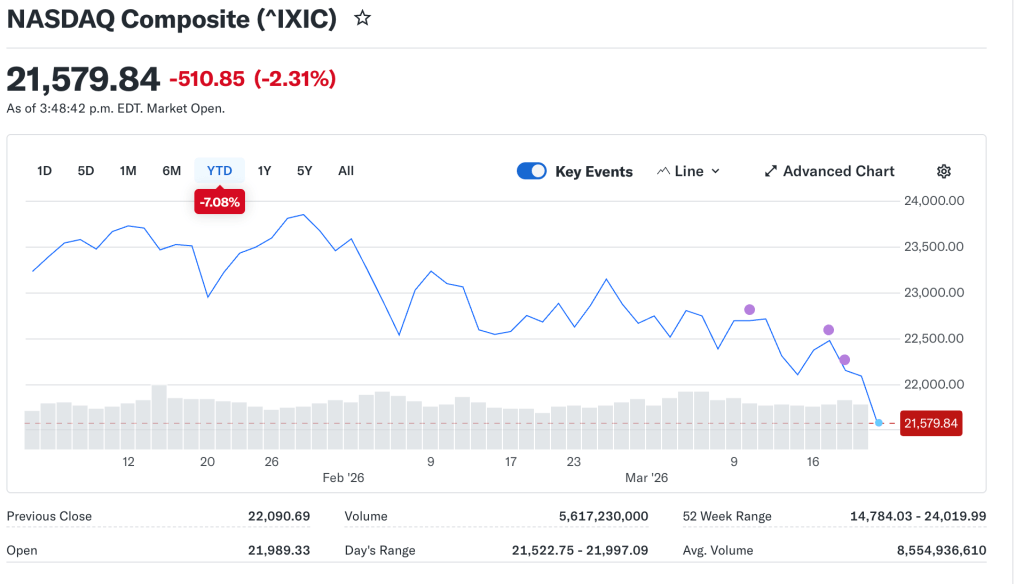

I get why people are nervous. Screens are red, headlines are loud, and every pullback suddenly feels like the start of something much worse. But honestly? I don’t really care that the TSX and Nasdaq are getting hit right now, because this looks a lot more like another correction of the market than the end of the story.

That does not mean the drop feels good. It means it feels normal.

The setup for a correction was already there. The TSX had surged into record territory earlier this month and, even after the recent selloff, it was still up more than 26% year over year as of March 20. Meanwhile, the Nasdaq-100 finished 2025 up 20.2%, marking its third straight year of double-digit gains. After that kind of run, a reset should not shock anyone. It should be expected.

Reuters reported that tanker traffic through the Strait of Hormuz had effectively collapsed after the Iran conflict escalated, and that kind of disruption hits global inflation expectations and rattles equities fast. But here’s the part I think matters most: panic usually prices in permanence, while markets usually deal in phases.

The war tied to Iran is serious, and the market is right to react to it. Oil shocks matter. Shipping disruptions matter. Inflation risk matters. But geopolitical crises do not last forever, and markets eventually stop trading the fear and start pricing the next six to twelve months instead. That does not mean the volatility is over tomorrow. It means today’s fear can become tomorrow’s opportunity.

So my view is simple: this correction was overdue after a powerful stretch through 2023, 2024, and 2025. The reaction we’re seeing now is not some unnatural event. It is what markets do. They overheat, they shake out weak hands, and then they hand long-term investors another entry point.

My 3 top TSX buys in this selloff

1. Canadian National Railway (TSX: CNR)

If I’m buying a correction, I want at least one high-quality compounder with durable cash flow and a business that can weather macroeconomic noise. CN fits that perfectly. In its January 30, 2026 release, CN said it delivered a strong fourth quarter and year-end 2025 result, backed by disciplined execution and operating efficiency. In a market correction, I like owning a core infrastructure name that does not need hype to work over time.

2. Enghouse Systems (TSX: ENGH)

This is a much more under-the-radar pick, which is exactly why it gets interesting in a selloff. Enghouse reported Q1 2026 revenue of $120.1 million, with recurring revenue of $84.6 million, representing 70.4% of total revenue. That recurring base matters. Even though growth has cooled, this is the kind of software business that can become attractive when the market gets too pessimistic and starts throwing out solid companies with sticky revenue.

3. Constellation Software (TSX: CSU)

Not every pick in a correction should depend on energy, banks, or the headline of the day. Constellation gives you a different kind of resilience. In Q4 2025, revenue rose 18% to $3.177 billion, and full-year cash flow from operations increased 24% to $2.732 billion. This remains one of the TSX’s best long-term compounders, and market pullbacks are often when investors finally get a more reasonable entry point.

Bottom line

I’m not treating this selloff like a reason to run. I’m treating it like a reminder. Corrections are part of the cycle. After huge gains, they are healthy. After fear spikes, they are usually uncomfortable. And for patient investors, they are often useful.

That’s why I’m not panicking about the TSX or Nasdaq falling. This appears to be another phase, not the finale.

Not personal financial advice, just how I’m reading this market.

Leave a comment