By Nicolas Frendo • April 8th, 2026 • 3 min read

The most disruptive part of a SpaceX IPO would not be the symbolism. It would be the scale. Recent reporting has described SpaceX as pursuing a mega-offering with proceeds reportedly up to $75 billion and a valuation target described variously as about $1.75 trillion or, in later reports, more than $2 trillion. In a global IPO market that raised US$171.8 billion in all of 2025, one transaction of that size would not just lead the year. It would dominate it. [1][2][3]

That is why a SpaceX listing could suck the life out of the rest of the IPO calendar. Portfolio managers do not have infinite attention, infinite liquidity, or infinite risk budgets. When a once-in-a-generation asset comes to market, everything else suddenly looks like an appetizer. Good companies may still list, but they risk being priced in the shadow of a giant that can soak up cash, headlines, analyst bandwidth, and retail demand all at once.

Venture Capital’s own problem

The same distortion hits venture capital from the other direction. Venture firms rely on public markets for markups, comps, and exits. If public investors become obsessed with one or two mega-stories, smaller growth names can find themselves stuck in valuation limbo: too expensive for sober public buyers, too unexciting for a market mesmerized by category-defining platforms. A blockbuster SpaceX IPO would not just create a winner. It could reset the benchmark for what feels worth owning.

Image 1. If SpaceX raises about $75B, that is roughly 44% of 2025 global IPO proceeds. [1][2][3]

That 44% figure matters because IPO markets are social systems. Momentum attracts more momentum. Underwriters shift attention to the biggest fee pool. Financial media reallocates coverage to the biggest spectacle. Hedge funds and long-only managers reserve cash because they do not want to miss the deal everyone will be judged against. The effect is not subtle. It changes the temperature of the entire market.

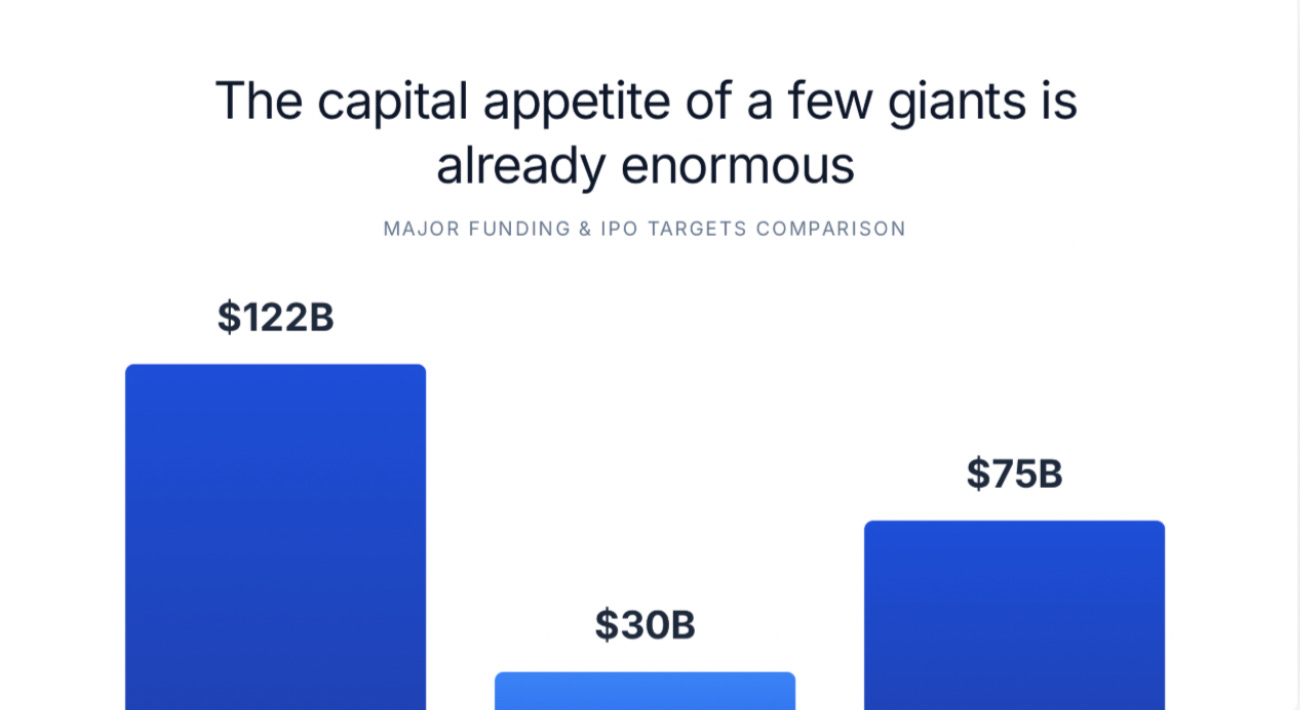

Now imagine the follow-on shock. OpenAI said on March 31, 2026, that it closed a $122 billion funding round at an $852 billion post-money valuation, and Anthropic said on February 12, 2026, that it raised $30 billion in Series G at a $380 billion post-money valuation. Neither needs to go public tomorrow for the pressure to build. Once one mega-issuer breaks the seal, the market starts asking why the other private titans are still waiting. [4][5]

“The danger is not just one giant IPO. It is the chain reaction that teaches every private titan to sprint for the same exit window.”

Image 2. Even before any IPO, the capital absorbed by a handful of AI and aerospace giants is already extraordinary. [1][4][5]

If SpaceX lists and trades well, the signal to late-stage venture capital will be clear: the exit door is open for giants, and maybe only for giants. That sounds positive until you consider the squeeze it puts on everyone else. More capital will chase fewer mega-winners. More founders will optimize for narrative scale over disciplined economics. More funds will hold their best names longer and starve the middle of the market.

If OpenAI or Anthropic also IPO in 2026, the problem compounds. Bloomberg reported on April 6, 2026, that both companies might go public this year, though neither company had formally announced an IPO at the time of writing. The calendar stops being a marketplace of many stories and turns into a referendum on a tiny number of superplatforms. That would be great theatre. It might even be great for bankers. But it would make the broader IPO market feel smaller, narrower, and more fragile than it already is. [2]

Re-Arrangement Theory

There is also a mechanical market-structure consequence. If SpaceX lists on Nasdaq, it would be competing for space in the Nasdaq-100, which Nasdaq defines as the 100 largest Nasdaq-listed non-financial companies. The index is reconstituted annually, uses a modified market-cap weighting scheme, and, under Nasdaq’s current methodology, eligible companies must have their primary U.S. listing on the Nasdaq Global Select Market or Nasdaq Global Market, meet liquidity and float requirements, and satisfy a seasoning period for initial inclusion. In plain English: a company as large as SpaceX would not just be another ticker. It could force a rapid reshuffling of index weights and passive flows, pushing smaller constituents down the ladder and pulling benchmark-tracking money toward itself. [6][7]

The S&P 500 effect would matter even more, but it is less automatic. S&P says the index covers roughly 80% of available U.S. market capitalization and notes that about $16 trillion was indexed or benchmarked to the S&P 500 in 2023. Entry is decided by committee, and the current eligibility framework requires a company to be U.S.-domiciled, large-cap, liquid, sufficiently floated, and financially viable; for the S&P Composite 1500, that means positive GAAP earnings in the most recent quarter and across the last four consecutive quarters, with the current S&P 500 market-cap threshold at US$22.7 billion. So the economic effect is a two-step process: first, a mega-IPO can crowd out attention and capital from other offerings; then, if it enters the major indices, it can redirect passive demand, research coverage, and even household retirement savings toward a single new giant. That is not just a stock-market story. It is a concentration story for capital allocation across the real economy. Now imagine it for two more this year, OpenAI and Anthropic [8][9]

References

- [1] Bloomberg, “SpaceX Said to Target as Much as $75 Billion in Blockbuster IPO,” March 25, 2026; and Bloomberg, “SpaceX Targets More Than $2 Trillion Valuation in IPO,” April 2, 2026.

- [2] Bloomberg, “Is SpaceX Worth $2 Trillion? Key Questions for Musk’s Big IPO,” April 6, 2026.

- [3] EY, “Global IPO Trends 2025,” published December 17, 2025. EY says 1,293 IPOs raised US$171.8b globally in 2025.

- [4] OpenAI, “OpenAI raises $122 billion to accelerate the next phase of AI,” March 31, 2026.

- [5] Anthropic, “Anthropic raises $30 billion in Series G funding at $380 billion post-money valuation,” February 12, 2026.6] Nasdaq, “Nasdaq-100 Index Methodology,” current methodology document (copyright 2025), including eligibility, selection, and weighting rules.

- [7] Nasdaq, “Nasdaq Concludes Public Consultation on Nasdaq-100 Index Methodology,” March 30, 2026. Nasdaq said the updated methodology becomes effective May 1, 2026.

- [8] S&P Dow Jones Indices, “The 500,” current overview page. S&P says the index covers approximately 80% of available U.S. market capitalization and that an estimated US$16 trillion was indexed or benchmarked to the S&P 500 in 2023.

- [9] S&P Dow Jones Indices, “S&P U.S. Indices Methodology,” current methodology document, including current S&P 500 market-cap guideline of US$22.7 billion and profitability criteria for the S&P Composite 1500.

Editor’s note: This piece is written as a forward-looking market commentary based on reported 2026 SpaceX IPO plans and current private-market funding levels. It is not investment advice.

Leave a comment